Mileage is one of the most important topics for personal auto insurance providers. The more miles a policyholder drives, the higher the risk of them having an accident. While laws differ between states, insurers in California are legally required to use estimated mileage as their second mandatory rating factor when calculating rates.

Even though mileage plays a big role in each and every personal auto insurance policy, insurers are collecting and using mileage in a number of ways. Many insurers allow policyholders to self-report their estimated or actual mileage, but both are often inaccurate. Some insurers exclude mileage from their rating factors altogether, resulting in even less precise underwriting and high risk for the insurer. As a result, underreported mileage causes personal auto insurers in the United States $5.4 billion dollars in losses every year, making the problem of mileage self-reporting too costly to ignore.

In this blog post, we’ll explore why insurance providers shouldn’t rely on mileage self-reporting and which alternatives they can use to verify their policyholders’ mileage to address a $5.4 billion annual problem.

The issue with self-reported mileage

What is self-reported mileage?

In order to classify customers into different rating categories, many insurers ask their policyholders to self-report their annual mileage. Policyholders are asked either to estimate how many miles they will drive in the next 12 months or to report how much they drove in the past 12 months. The policyholder’s insurance premium or renewal premium will then be calculated and/or adjusted based on the reported number.

Estimated mileage

Insurers might ask policyholders to self-report their estimated mileage in different ways. For example, insurance agents might call policyholders and ask them how much they anticipate driving within the next 12 months. Others might send policyholders a form to fill out and mail back to them, or they might offer online services that allow policyholders to submit this information via email or through a web portal.

Actual mileage

Instead of, or in addition to, estimated mileage, some insurers ask their policyholders to self-report how many miles they drove in the past 12 months. The most common ways to collect this information are the examples mentioned above, as well as the option for policyholders to take a photo of their car’s dashboard and send it to the insurer.

Why is self-reported mileage problematic?

No matter whether insurers ask policyholders for their estimated or their actual mileage, all mileage self-reporting causes major disadvantages for insurers and policyholders alike.

Inaccurate data

First and foremost, self-reported mileage is often inaccurate and causes insurers to incorrectly price and underwrite their policies. Over half of policyholders underreport their mileage to insurance providers every year. A quarter of drivers understate their annual mileage by 6,000 miles or more, and 16% even think that it is acceptable to lie to their insurer about how many miles they drove. These inaccuracies lead to errors in pricing and underwriting, which we’ll discuss in the section below.

High cost

Apart from yielding inaccurate results, collecting self-reported mileage information is expensive for insurers. For example, when agents call policyholders to collect mileage estimates over the phone, they need to repeat this process for each policyholder every year. This makes mileage self-reporting extremely labor and cost-intensive, especially considering that some policyholders don’t pick up or don’t have an estimate at hand on the first phone call.

Poor user experience

While collecting self-reported mileage is a lengthy and costly process for insurers, it also creates a suboptimal user experience for policyholders. No matter how fast and easy insurers try to make this process, mileage self-reporting still causes an inconvenience to each and every policyholder. Let’s be honest —nobody wants to spend time keeping logbooks, calculating how much they drive, or taking photos of their dashboard. It is understandable that so many policyholders end up reporting incorrect numbers.

How does self-reported mileage impact pricing, underwriting, and customer retention?

Unfortunately, the problems and disadvantages mentioned above go beyond inaccurate data, costly processes, and unhappy customers. Self-reported mileage also negatively affects an insurance provider’s pricing, underwriting, and customer retention.

Imprecise pricing

As self-reported mileage is notably inaccurate, insurers have no choice but to establish broad risk categories that leave room for errors. The problem is that mileage is in fact an important risk factor. For example, policyholders that drive under 3,000 miles per year file 44% fewer claims than the average. Policyholders that drive over 20,000 miles file 28% more claims than the average. With a risk factor this important, choosing too broad risk categories leads to highly imprecise pricing structures.

Incorrect underwriting

While self-reported mileage makes actuaries unable to define adequate risk categories, it also makes underwriters unable to correctly evaluate each policyholder’s risk. These overlooked underwriting practices result in wrongly calculated rates and $5.4 billion in premium leakage losses for American insurers every year.

Low customer retention

Ultimately, an insurer’s erroneous pricing and underwriting causes customers to be unsatisfied and eventually switch to another insurance provider. Underreported mileage, combined with other types of premium leakage, causes policyholders to pay on average $400-700 more per year for their auto insurance premium. Among drivers that are shopping for a new insurance policy, 64% cite price as their primary reason for switching to another insurance provider.

Alternatives to mileage self-reporting

Clearly, insurers need to find a way to replace mileage self-reporting and gain back the $5.4 billion in premium leakage they lose each year. Luckily, there are ways for insurers to instantly and easily verify their policyholders’ mileage without compromising accuracy, cost-efficiency, or a good user experience.

OBD-II dongles

Some insurers encourage policyholders to install aftermarket hardware devices like on-board diagnostics (OBD-II) dongles in their vehicles. Those devices allow the insurer to track miles driven as well as other information, for example, the vehicle’s location. This solution is most common among insurers that offer pay-per-mile insurance policies, which charge policyholders by the mile.

Smartphone telemetry

Instead of using a third-party device, other insurance providers allow policyholders to opt into tracking their mileage, location, and driving behavior via their own smartphone. This solution is especially popular for usage-based insurance (UBI) programs, which charge policyholders based on how they drive and how much they drive.

Unfortunately, smartphones are often inaccurate when it comes to tracking mileage. For example, smartphones erroneously detect trips when the policyholder is riding in someone else’s car. They also fail to record any data in areas with poor cellular coverage.

Third-party data sets

Among insurers that offer neither pay-per-mile nor UBI programs, the most common way to verify a policyholder’s mileage is by purchasing third-party data sets that contain vehicle history information such as mileage, ownership record, and accidents.

The problem with third-party data sets is that they aren’t always accurate and updated with real-time information. While they can be useful to verify other information, they might not be the best way to verify mileage.

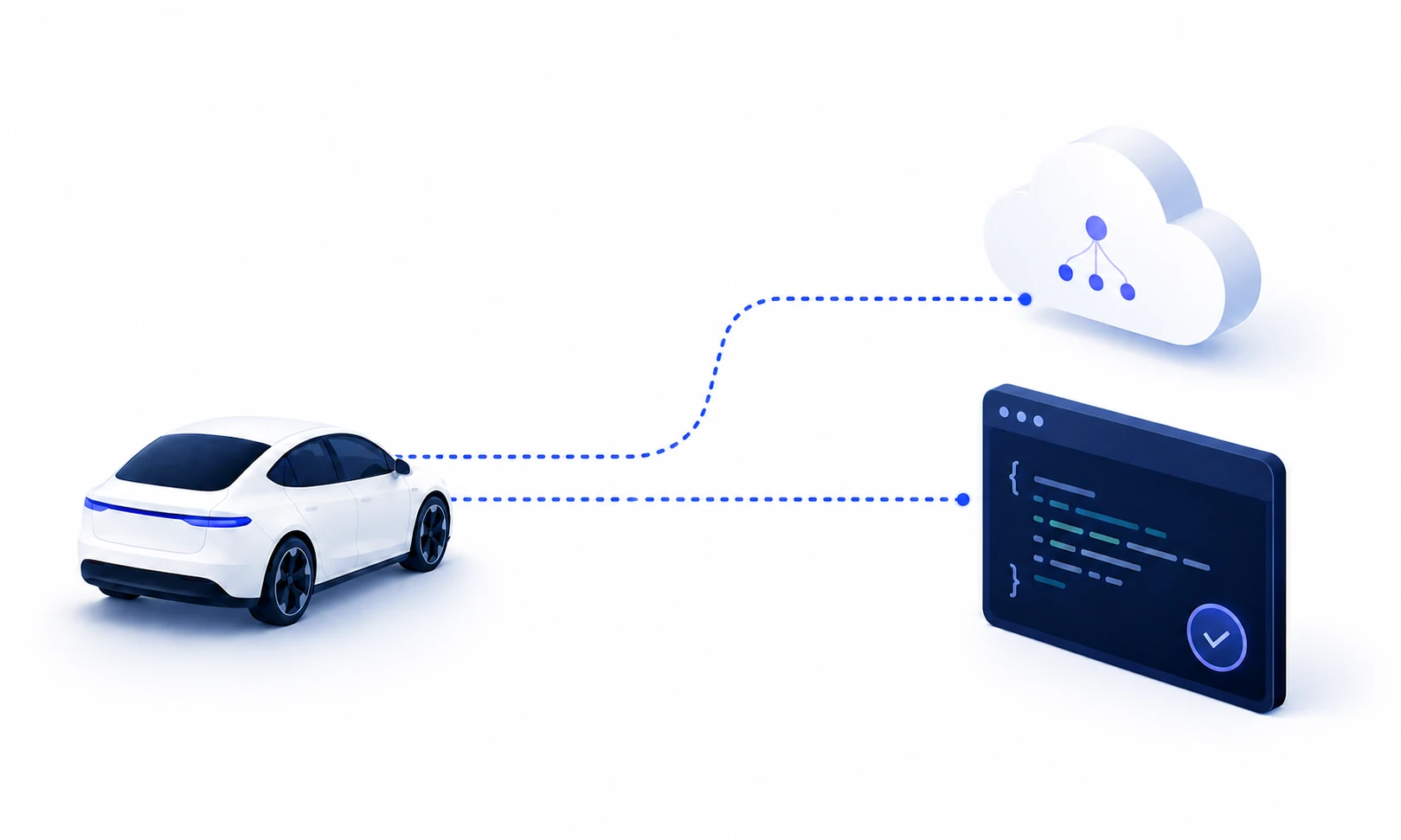

Car APIs

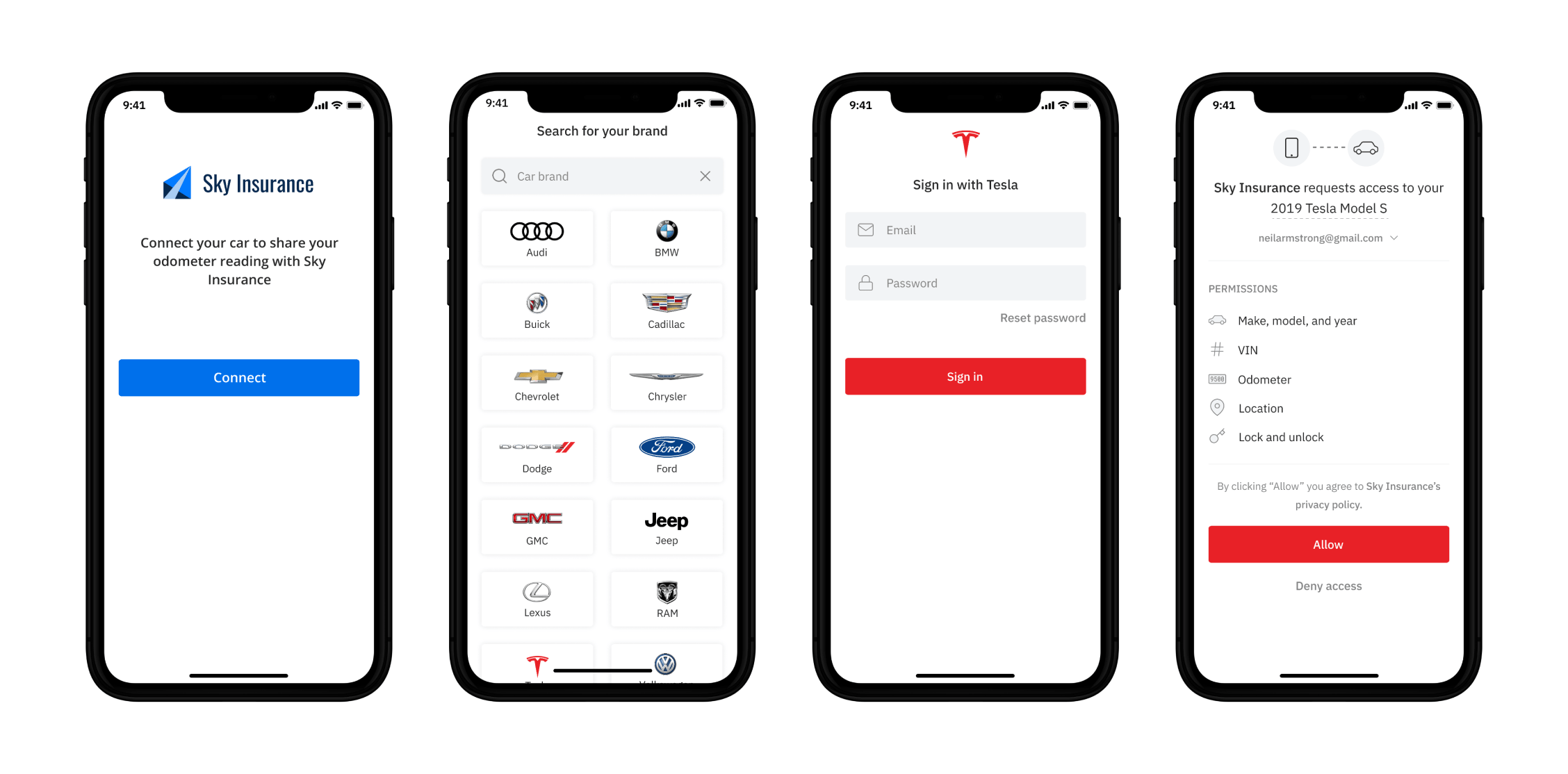

API platforms like the Smartcar API are becoming more and more popular among insurers that offer traditional insurance programs, pay-per-mile programs, or UBI programs. The Smartcar API allows policyholders to link their vehicle to an insurer’s mobile or web application. The policyholder agrees to share specific vehicle telemetry, such as their mileage, location, and VIN. The insurer then retrieves this information as often as needed using simple API requests.

The advantage of using API technology for mileage verification is that it is instant and accurate. Smartcar’s technology integrates directly with each vehicle’s cellular modem to retrieve its mileage directly from the instrument cluster. There is no need for third-party devices or data purchases. This makes car APIs like Smartcar cost-effective as well as easy to use and maintain for policyholders and insurers.

Finally, Smartcar allows policyholders to quickly and easily opt in to sharing their vehicle’s information with the insurer. Policyholders can link their vehicle with just three clicks. They have transparency around exactly which types of data they are sharing and why. This allows insurers to offer a smooth customer experience, all while respecting their policyholders’ privacy and trust.

All in all, a mileage verification solution can get costly and hard to implement without the proper systems in place. Smartcar’s API technology instantly and accurately informs an insurer’s pricing and underwriting processes, increases customer retention, and addresses the $5.4 billion annual premium leakage problem that insurance providers face every year.